2026 – Q1 Market Update

2026 – Q1 Market Update

Dear Clients and Friends,

We hope you enjoyed the holiday season with the ones that matter most. Everyone at Vance Wealth is energized as we begin the New Year, and we’re focused on guiding clients through markets with clarity, discipline, and confidence.

2025 Market Performance

Last year was the third year in a row of double-digit market returns. The S&P 500 returned +17.88% and International Developed Markets were +31.85%, significantly outperforming US companies on a broader scale. The US Bond Market was +7.30%, even the more conservative assets had a strong growth year. Corporate earnings remained resilient, and many companies continued to grow profits despite an evolving economic backdrop. Inflation continued to ease compared to prior years, which helped strengthen investor confidence and improved expectations for longer-term stability. In addition, the Federal Reserve began shifting toward a lower interest rate environment, which can be supportive for both business activity and market valuations. We saw continued strength in innovation-led areas of the market, particularly as advancements in technology and artificial intelligence remained a meaningful driver of growth. I’ll have more on the later…

2025 was a reminder that markets don’t move in a straight line. The year started with meaningful volatility – between January 1st and April 8th, the S&P 500 declined nearly (15%), while international markets held up relatively well, down just over (3%). During that period, we had important conversations with many clients about staying disciplined and remaining committed to long-term financial plans, even when headlines and uncertainty can create discomfort. While the early part of the year was challenging, it reinforced a key truth of long-term investing: strong decision-making and steady discipline during difficult stretches can make a meaningful difference over time. Looking back with hindsight is the easy part. But, we now know the market weakness was temporary and the investors that stayed committed were rewarded in the end.

With gold and silver posting impressive gains in 2025 (Gold: +57.49% – Silver: +152.68%) along with strength in other areas like copper, which has been supported by increased demand tied to AI and infrastructure investment – it’s understandable that commodities are receiving a lot of attention and excitement from investors. However, it’s important to keep these strong short-term results in perspective. Even though the Bloomberg Commodity Total Return Index was up around 15% in 2025, it produced a negative annual return over the past 15 and 20 years. For that reason, while commodities can absolutely have a role in a well-diversified portfolio, we believe they are best used as a complement to a long-term strategy rather than a concentrated holding.

With 2025 in the rearview mirror, there are 3 core tenants that we believe investors should live by that will set you up for success in the future.

- Volatility is normal, abandoning a plan is not

- Diversifying is about preparing not predicting

- Discipline matters more than timing

2026 – Entering a Market Based off Fear and Optimism

Areas of Concern

- Valuation Stretched ➜ Markets are more expensive (Price to Earnings) on a historical basis.

- The last time valuations were this elevated, this was before the dot com bubble. We are not at the same level, but something to keep an eye on.

- We believe we will continue to see earnings growth to justify these higher valuations.

- Rising Unemployment ➜ Growing concern. If this persists, this could make the case for the FED to continue cutting rates. This could help stimulate the economy.

- Federal Finances ➜ The government has a spending problem. Our hope is to get rid of fraud and waste in the system. We expect an uptick in productivity and economic growth to help work our way out of this deficit.

- Tariffs ➜ Elevates the amount of uncertainty. It is hard for business owners to make long-term decisions.

- Reciprocal Tariffs make things fair and helps us bring back US manufacturing. We saw how exposed we were during COVID and relying too heavily on imports.

The Case for Optimism

- Earnings Acceleration ➜ EPS is projected to grow double digits in 2025 – 2027. EPS growth from 2001 – 2024 has been approximately 7%.

- Tax cuts that occurred in 2025 that unlocked a lot of growth for corporate America.

- Productivity boom from AI should continue to propel this forward.

- Inflation Cooling ➜ Technology is deflationary. We are seeing prices come down and we are seeing this in the data, but maybe not in the media.

- Healthy Consumer ➜ Consumer is healthy in aggregate when you compare to government financial health and spending.

- Compounding ➜ If you invested in cash in 1996, you lost money from 1996 – 2025. It is great for emergencies, but it is not great for investing. This continues to make the case for investing in equities when you have time on your side.

- Diversification Certainty ➜ If you have time on your side, the probability of success goes up that you achieve positive returns with a diversified portfolio.

Are we In an Artificial Intelligence (AI) Bubble?

While we understand the skepticism, we don’t believe that’s the right conclusion. At least not yet. In our view, we are still in the early stages of AI adoption, with many companies just beginning the buildout and investment required to integrate AI into their businesses. Short-term fears may prove to be overblown, though that doesn’t mean the path will be smooth – periods of volatility are likely, and we believe those pullbacks can create attractive long-term buying opportunities. We’re also seeing market returns begin to broaden beyond a handful of large technology companies, in part because of the significant capital spending required by hyperscalers to support AI infrastructure. Importantly, the long-term opportunity extends beyond simply improving existing business lines. As AI becomes more deeply embedded across the economy, we believe it has the potential to unlock entirely new sources of revenue in technology and many other industries -though exactly where those opportunities emerge remains uncertain. Remember when the internet became a thing? People were worried about losing their jobs. And some did. BUT, think about how many NEW jobs were created.

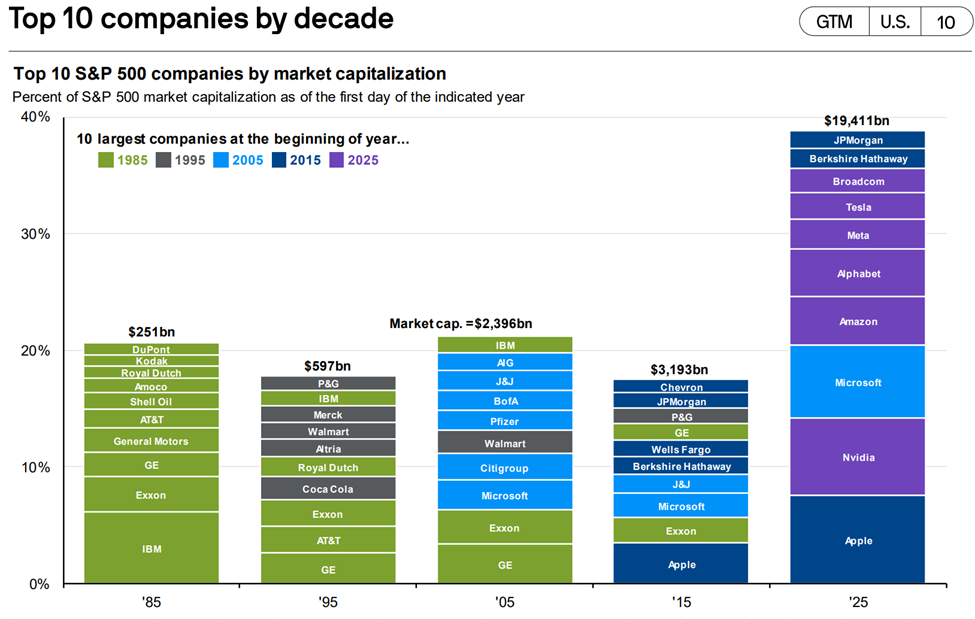

Market Leadership does not last forever. In the graph below1, this shows the 10 largest companies at the beginning of the year in 1985/1995/2005/2015 and 2025. While we love so many of the current 10 largest companies, when you look back 10 years ago, there is no Tesla, no Amazon, no Nvidia. This was only 10 years ago! If you go back 20 years ago, only Microsoft is still on this list.

This shows how important diversification really is. We have great American companies that sell amazing products, grow their profits, and grow their earnings. This list has changed so much over the past 40 years, and will likely look different in the next 10 years. We have to prepare for this and is why we should not concentrate our investments in the current “winners” today.

What We’re Focused On at Vance Wealth

- Helping investors stay disciplined through uncertainty.

- Ensuring portfolios remain diversified and aligned with long-term goals.

- Making thoughtful adjustments when needed – without reacting emotionally.

In markets like these, our role is simple: Provide clear, informed guidance so investors can make confident decisions.

If you would like to discuss your long-term financial plan in greater detail or would value a review of your current investments, please get in touch with our office to schedule time with one of our Wealth Advisors. If you are not currently a client and value a second opinion, we are here to help. Now is a better time than ever to look at your current investments and financial plan to make sure they are properly positioned for the unexpected.

Regards,

Jerrod Ferguson, CFP®

Partner

Sources:

- Source: Bloomberg, S&P Global, J.P. Morgan Asset Management. Companies are organized from highest weight at the bottom to lowest weight at the top.

Disclosures: The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. Past performance does not guarantee future results. The information provided is for educational and illustrative purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. Vance Wealth, LLC. (“Vance Wealth”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Vance Wealth and its representatives are properly licensed or exempt from licensure. The S&P 500 is an unmanaged index of 500 widely held stocks. Investors cannot invest directly in an index.